LendingTree is an industry-leading search, comparison and recommendation engine for consumer financial services. We’ve built tools and services that have helped save our users billions, and now you can do the same.

We’ve got a comprehensive developer-friendly suite of feature-rich modules, including a complete API and SDK toolkit. Our easy-to-use platform provides everything you need to integrate holistic financial awareness tools directly into your users experience.

Our distributed, accessible solutions cover the entire financial ecosystem, including credit cards, loans and insurance. They can provide the data to enrich and enhance your existing offerings.

View a full list of our services.

Personalized credit score, credit file details, analysis of credit factors plus credit monitoring that keeps customers informed.

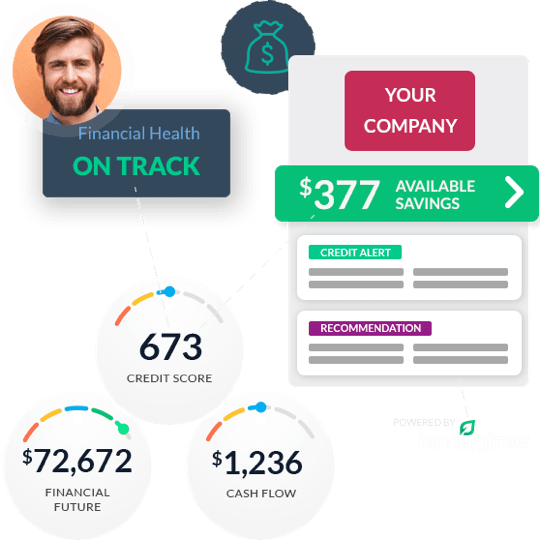

Intelligence platforms for savings alerts, credit advice and financial recommendations.

Identify valuable savings opportunities for users that can help them cut payments and build wealth.

Help users understand and act on trends from their own credit and asset data with smart, actionable insights.

Give users access to an ever-increasing library of easy-to-digest educational videos.

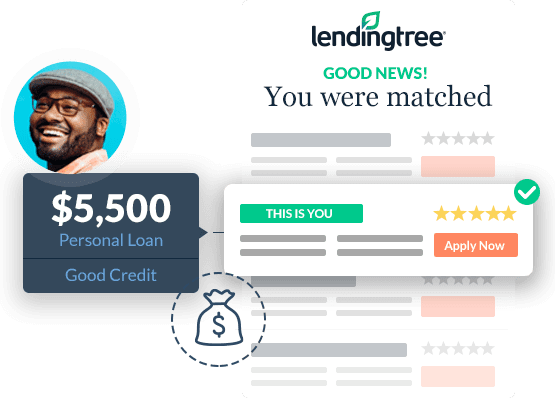

Enable any financial product in the LendingTree network for your users. “Turn on” the products that matter most.

We offer fully integrated a la carte solutions. It’s always your brand, just our tech under the hood.

Over 20 years ago, LendingTree brought mortgage shopping online. Since then we’ve pushed the industry forward developing online solutions for loan shopping, credit improvement, debt reduction, auto financing and so much more. With the nation’s largest network of lenders, we’ve become the go-to place to shop for money.

LendingTree used this same tech to build a subscriber-led, savings-centric product that engages, monetizes and delights customers over their entire lifetime of financial transactions. What will you create?